ASML is not ridiculously expensive: 3P-Check

We are looking at the most popular stocks currently on the market and examining whether investors' expectations are realistic. We are conducting the 3P Check, this time focusing on ASML. Both supporters and critics agree that this is a great company, but is the current price justified?

For those reading this for the first time, here's a reminder of what the 3P Check entails. If you are already familiar with the 3P Check, you can skip the following section.

What is the 3P-Check?

One of the goals I set for myself with Valuing Dutchman is to be a voice of rationality in the stock market, advocating for calmness both during panic and euphoria.

The term 3P refers to "Possible, Plausible, and Probable" from Professor Aswath Damodaran's book "Narrative and Numbers," also known as the "Dean of Valuation." The aim of the book is to learn how to link numbers to stories and vice versa.

We will examine the valuation of a company in the market and ask ourselves:

Is it Possible? Does the story that the current market price tells even have the potential to occur? Can a company truly grow that strongly, increase its margins, and so on? You would be amazed at how many impossible stories exist.

Is it Plausible? Technically, it may be possible, but is it believable? Are the expectations realistic? Are there past examples that support these stories and expectations?

Is it Probable? Is it likely that the narratives associated with the current stock price will unfold as projected? The difference between this step and the previous one heavily relies on the analyst's beliefs. At this point, I often find myself in disagreement with others.

The goal is to pause and reflect on market prices, using historical data alone to determine in which of the three P's I believe this price falls. I also perform a quick calculation of what I would be willing to pay for the company in question.

Please note, this is not an in-depth analysis or a comprehensive valuation of the company.

ASML

After reviewing NVIDIA last time, I found it interesting to take a closer look at the company leading the Dutch AEX index.

ASML specializes in the development and production of advanced lithography systems for the semiconductor industry. Their innovative machines are crucial for manufacturing integrated chips used in a wide range of electronic devices such as smartphones, computers, and automobiles. ASML is renowned for its groundbreaking technologies, including extreme ultraviolet (EUV) lithography, enabling the production of increasingly smaller and more powerful chips. The company plays a vital role in the global semiconductor supply chain and collaborates closely with all major chip manufacturers.

ASML's growth over recent years has been remarkably strong. Revenue has grown at a rate of 16.3% annually, and earnings per share have increased by 19.9%.

ASML not only managed to increase its revenue but also improved its gross margin during this period. Additionally, the company bought back a significant amount of shares, while reducing its debt level considerably.

What more could we ask for?

We simply want to know if we are not overpaying for this wonderful company today. If something is priced to perfection, there's little room for positive surprises, and any negative surprises could push the stock price lower. But is that the case here?

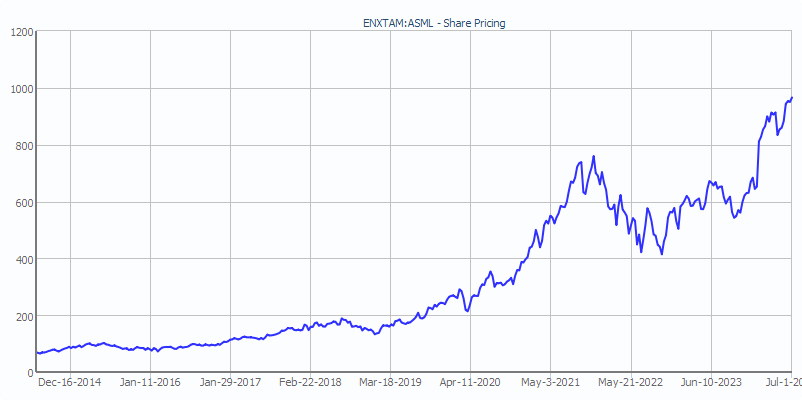

Here is the stock price over the past ten years.

What is the market expecting?

Based on the current stock price of €988, we can calculate what the market expects in terms of returns based on historical growth rates, or what growth is necessary to meet a return requirement of 12% through a reverse discounted cash flow calculation.

With a required return of 12% (discount rate), ASML would need to grow its cash flow from the last fiscal year (2023) by 35% annually over the next ten years. There have been periods where cash flow grew faster, but not consistently over such a long period—typically in five to six-year periods. Over the last decade, cash flow grew at an average rate of 16.8% per year.

However, the last year experienced a dip in cash flow. Excluding this weaker year and considering the nine years prior, the growth rate averages 29.9%, which is closer to the targeted 35%. Yet, achieving a 12% return seems challenging at the current stock price.

If we consider the potential return at the current stock price based on the growth of 29.9% over the nine years up to 2022, we might expect a return of 9.6%. With a growth rate over ten years of 16.8%, the expected return would be 5.4%. Especially the latter figure is insufficient for a risky equity investment, even in a strong company.

We can apply the same approach to earnings per share instead of cash flow. Earnings per share are typically less volatile because major investments are spread over time, thereby less influenced by single-year impacts. But is also easier to manipulate.

Using the latest fiscal year's earnings per share, only an 8% growth per share is needed to achieve a 12% return, while earnings per share have grown by 19.9% over the past ten years. Although 2023 may have been an exceptional year, previous periods show that a growth rate of 14.8% is achievable. There might be a year or two where growth slows after the exceptional year of 2023, but a growth rate of 8% appears feasible given ASML's history.

How will the future unfold??

All the above analysis is based on ASML's historical data. But what about the future? Will competitors emerge with equally good or even better machines, potentially putting pressure on ASML's revenue and margins?

In the history of capitalism, it has always been the case that high margins and prices for products eventually lead to solutions for those high prices. Either demand decreases due to high prices, or competition increases, thereby increasing supply, leading to price declines.

I'm not an expert in ASML or this type of machinery, but based on what I've seen and read so far, it appears that competition still lags behind ASML and a catch-up is not yet in sight.

Of course, the immense demand for these machines could decrease if the demand for chips declines, or if technological innovation slows down, allowing the same machines to be used for longer periods. Only time will tell how this will unfold.

What would I want to pay?

Given my background in a sector that has experienced significant disruption (photography, IT, and telecom), I am biased and will likely never own companies like ASML unless I can buy them at what experts consider a ridiculously low price.

However, the most important thing in investments is my peace of mind, which I only have when I feel comfortable with the price I've paid.

For ASML, I arrive at a price I'm willing to pay of €540, based on a slightly lower base earnings per share of €14 (matching 2021 and 2022) and a growth rate of 5% per year from that point onward. I understand this approach is very conservative, but I am exceedingly cautious in rapidly changing sectors, even though ASML has proven its ability to lead through these changes.

Are expectations realistic?

While ASML is certainly not a bargain on the stock market, we can't help but conclude that it falls solidly into the second P (Plausible) of Damodaran's framework. It's plausible that ASML can meet expectations. I would even go further: purely based on historical figures, it is likely (Probable). However, I prefer to leave that assessment to industry experts.

As I mentioned earlier, I am more cautious and would only buy with a significant margin of safety and after thorough research.

Quality comes with a price. I bought ASML during the market dip in October 2022.

At that time it could also be considered expensive with a P/E ratio around 30, but that didn't stop the share price from doubling since then.

I couldn't predict the AI hype, but I saw the unique position of this company and the increasing worldwide demand for semiconductors.

So yes, today even more people can only agree that this stock is expensive and priced to perfection. I'm not adding to my position at the current valuation, but it would've been better to have this kind of analysis a few years ago.

Interesting to take what is more or less the approach to classifying oil and gas reserves and applying it to the prospects of a given company.