Weekly: Terrifying

Weekly 35 2025

This week

Over the past two holiday weeks, several companies have presented their numbers. We've already looked at:

Under Short News you'll also find updates on F.I.L.A and Bellway, plus a short message about Somero Enterprises.

Terrifying

We all know that Donald Trump likes to play 'games' to get his way. In the case of Intel, he first accused the CEO of having too close ties with China and demanded his resignation, which caused Intel’s stock price to drop.

Trump then used this stock drop to force the company to convert a large subsidy from the Biden administration into new Intel shares. This way, he claims to have received the shares 'for free,' earning the United States $11 billion. In practice, this amount was simply stolen from existing shareholders. The market, however, doesn't seem to care, as the stock price has risen.

This goes beyond the wildest dreams of the socialists in Belgium, who limit themselves to taxing 10% of the capital gains, not the full ownership.

Now that this stunt has proven successful, it's plausible he will undertake more of these actions. Not to mention other insiders who jumped on this and became significantly richer. After the 'Trump and Melania coins,' this is another flagrant example of market manipulation by the American president.

What's happening here is terrifying. It's appalling that there isn't more resistance from the press and shareholders. In my opinion, this is a result of an overheated market and the concentration of power among a few large parties through their 'passive funds.' These parties have no incentive to resist this, unlike a normal owner. Instead, they have a lot to lose from the application of normal regulations on their funds, which is why they remain silent and let Trump have his way.

Not that this is the only concern: his attack on the FED, the American central bank, is equally unprecedented. When you consider all of this, along with the other firings and appointments, the situation is more reminiscent of Russia than the United States.

Market Overview – August

I've been warning about the expensive US stock market for so long that it almost feels pointless to bring it up again. After all, what's expensive can always get more expensive. That’s why I was glad to read Howard Marks' August 13th memo, in which he stated that he now sees the market as not just "elevated," but "worrisome."

He does note that while all indicators point to an overvaluation, it can never be fully proven, and there's no guarantee of a short-term correction. After all, in addition to the many arguments for an expensive market, there are always reasons that justify the high valuation. Without those arguments, the market would never become so expensive in the first place.

Today, the main argument is that artificial intelligence (AI) will change the world. I completely agree, but I am certain that its impact on the stock market will be different from what most people currently expect.

Other arguments are that the current top companies are growing fast, are less sensitive to economic cycles, and require less capital to grow. This allows them to generate more cash flow and have a wider 'moat.'

However, with current valuations, they will need every inch of that moat to sustain their growth and justify these prices. And for some companies, it will indeed be 'different this time.'

But if history is any guide, the winners are rarely the companies everyone has their eye on now. Just look at the largest companies from 30 years ago and see how many of them are still at the top today.

How long the party will last is a completely different question. A week? A month? A year or longer?

As a value investor, I rely on the difference between value and price. I believe that in the long run, the price always moves towards the value. And with that in mind, I see more and more reasons to be cautious.

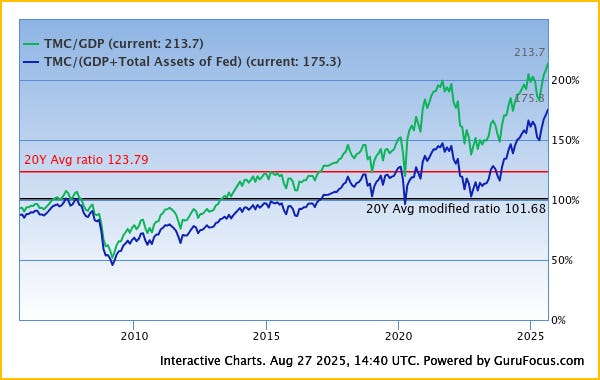

Meanwhile, the 'Buffett indicator' continues to climb to unprecedented heights.

Howard Marks also noted that because there are fewer IPOs and companies are staying in the hands of private equity for longer than they used to, this indicator is actually even more worrisome than the figures suggest. That’s because these companies are counted in the GDP, but not in the market capitalization.

Transaction Doubler Portfolio

Keep reading with a 7-day free trial

Subscribe to Valuing Dutchman to keep reading this post and get 7 days of free access to the full post archives.