VD 112: Consistently not stupid

In this issue:

Consistently not stupid

Stock in focus: Jet2

The Rationality Test: Lightwave Logic

What I’ve been reading these past few weeks

News from our companies

Doubler Portfolio update

Before we get started, a quick heads-up: I’m taking a week off to recharge the batteries. The next issue will be out on May 14th.

Consistently not stupid

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.” - Charlie Munger

Charlie Munger produced quite a few one-liners over his incredibly long career, but the one above is, for me, the one that best fits the current market. We are seeing those strange antics resurface that are so typical of a bull market.

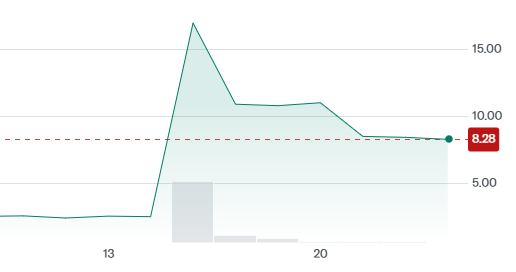

For instance, we saw Allbirds, a company that produced wool sneakers, sell off its operations for $39 million—a mere 1% of what investors paid at the time of the IPO. At the same time, the company announced it would invest this amount to transform itself into an AI firm. No products yet, just an idea. Even so, the share price jumped from $2.49 to $23.

You would expect investors to be less than accommodating toward a management team that has lost half of its revenue since the IPO and was essentially on the brink of bankruptcy. While the share price has since been divided by nearly three, at $8.43, it is still 3.4x higher than it was before the announcement.

This smells a lot like the dot-com era, back when simply slapping “.com” onto a name was enough to send a stock price through the roof.

We’re seeing some other strange things happening too. Take Avis, for example—a car rental company sitting on $25 billion in debt—which skyrocketed by a staggering 600%. This happened because two funds managed to buy up more than 100% of the shares, using a mix of common stock and derivatives. The end result? Short-sellers, who sell shares today hoping to buy them back cheaper later, suddenly couldn’t find any stock to cover their positions. The math simply didn’t add up anymore.

Those are some nice anecdotes, of course, but what’s happening in the broader market is actually beyond belief.

We are currently navigating an environment where the leader of the world’s largest economy has proven to be an unreliable partner to all other nations for over twelve months now. That fact alone should be weighing on the economy.

On top of that, we still have the ongoing wars in Ukraine and Gaza, with the conflict in Iran added to the mix. While the markets seem to have priced in the disruptions from the first two, the impact of the war in Iran is far from settled. It’s staggering to see the world index trading higher than it was before the Iran conflict broke out, especially knowing that oil supplies are disrupted and prices remain high. This is going to squeeze consumers and businesses globally. The longer it drags on—and we’re already more than 50 days in—the worse the impact will be. There’s no sign of a solution on the horizon, either.

I don’t think I need to pull up the usual chart of the Buffett Indicator anymore; by now, you understand all too well that we’re in exceptional territory. On one hand, there’s a very real threat to the global economy; on the other, stock markets are looking extremely expensive.

The argument I often hear and read for why these high indices and prices are justified is the earnings growth of American companies. That surge in profits will indeed happen. AI investments are a major driver for the bottom line of certain players. Take NVIDIA as an example: their profits will almost certainly see another spectacular rise this year, provided customers actually follow through on their orders.

However, what counts as revenue for NVIDIA is a cost for their customers—a cost that, for now, isn’t being offset by sufficient revenue. You might think this is a zero-sum game, where one’s profit is another’s expense, but that’s not how accounting works. NVIDIA books 100% of the sale as revenue, while the buyers of those chips depreciate them over, say, six years. Consequently, they only record about 17% as an annual expense. This effectively causes the combined profit of this group of companies to be overestimated by 83%.

I realize this is a simplification and that other factors are at play, but it illustrates the underlying mechanism. What applies to chips applies even more drastically to the construction of data centers (with depreciation over 20 years, or just 5% cost per year) and everything else involved in the rapid build-out of AI.

Despite the fact that markets are generally expensive, that certainly doesn’t apply to every individual stock. You just have to make sure you don’t do anything stupid. How do you avoid “doing stupid things” as an investor? By using logic and performing valuations. While a valuation always involves assumptions and will never be pinpoint accurate, it at least forces you to think those assumptions through and provides a necessary roadmap.

Keep reading with a 7-day free trial

Subscribe to Valuing Dutchman to keep reading this post and get 7 days of free access to the full post archives.