The profit will come on its own, right?

Week 44 2024 + Market update + planned transactions Doubler Portfolio

It’s the same story every month in the market overview: the U.S. stock market remains expensive. Too expensive.

The so-called Buffett Indicator keeps climbing; it’s fascinating to see how high it can go.

The Shiller PE is also approaching its all-time peak. The only thing keeping us from reaching the levels of 2000 is that back then, many companies were absurdly overpriced without making any profit. Today, that’s different: the most expensive companies are also profitable.

However, that profit isn’t enough to justify current prices. Still, people consistently point to the expected growth.

We’re not far off from the highest point in the last twenty years. The average over that period is already 50% above the long-term average since the beginning.

I hope for all ETF investors that we revert to the average of the past twenty years; in that case, the S&P 500 would ‘only’ drop by 29%. But if we go back to the historical average since the start, the index would have to drop by more than half.

I keep saying it: this is truly a market with two faces. This is also clear from our extensive selection list of worthwhile stocks. On the one hand, I’m optimistic about the opportunities emerging, but on the other, I’m concerned for those who don’t do their homework.

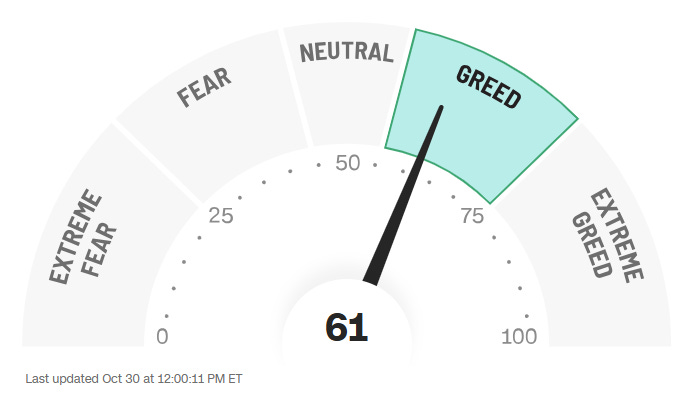

CNN’s Fear and Greed Index is back to showing "Greed" for the entire market, including the cheaper small-cap companies. This is a drop from a score of 67 compared to last month.

I’ll keep saying it: this is not a normal market. The concentration in a few companies is too high, and these companies are far too expensive. It seems inevitable that investors will eventually wake up and realize this won’t deliver the returns they’re hoping for.

They are, after all, being warned. Bank of America conducted a study showing that the S&P 500 is overvalued on 19 out of 20 measured factors.

The expected return for the S&P 500 according to this study is 1% to 2%, including dividends.

The responses I got on X illustrate today’s mindset perfectly. When I posted something about “Investing a lifelong journey”, someone replied: “You’re better off investing in an S&P 500 ETF than in Sofina; it takes no effort, and the return is higher.”

This is factually incorrect and a classic case of recency bias, where short-term performance is seen as the norm. Over the past 25 years, Sofina has outperformed the S&P 500, even now with Sofina undervalued and the S&P 500 overvalued.

When I pointed out on X that despite recent tough years, I’m still satisfied with a compound annual return of over 11% over 20 years, someone replied: “Just invest in the index if you’re happy with 11%.”

However, the S&P 500 achieved 9.54% over the same period, including dividends—and that was an exceptionally strong period for the index, while my portfolio went through a few weaker years.

It’s also worth noting that the S&P 500 currently has a price-to-earnings ratio of 29.7, whereas my portfolio stands at 8.4. That discrepancy can’t be justified by higher growth or lower risk.

These anecdotes from the past week painfully highlight today’s investor sentiment. Rationality seems to have vanished; people expect returns without effort or commitment.

Articles and updates this week

This past week, we received earnings reports from Bonava, X-Fab and Cloetta..

Read the Bonava update: At the Turning Point?

Read the X-Fab update: At the end of the whip

Read the Cloetta update: Sometimes the market agrees with you fast

On Tuesday, a short article was published: Investing a lifelong journey.

On Wednesday, no new stock was ultimately added. At the last minute, Danaos turned out to be just not quite good enough, especially compared to the companies in our portfolio. Instead, I shared a top five from our selection. Read the article First and Foremost an Investor here.