Greed or extreme greed? Depends on where you look.

update week 39 2024

For now, I tend to repeat myself a bit each month. Also, the overall state of the markets doesn’t matter much when you focus on individual stocks. However, if the market crashes, even cheap stocks will go down. But I gave up trying to time the market 20 years ago.

You could say that what we do—buying deeply undervalued stocks—is a form of timing, but based on fundamentals rather than price movements.

In the U.S., the market keeps moving higher. The chart below shows how far this stretch has gone. We can see from the green line that the GDP, the added value created by all companies, is growing; companies are generating more revenue and profit.

For a while, it was said that the greater rise in the stock market’s value was due to the FED increasing its assets by printing money. But now, we see that red line falling, while the blue line reaches unprecedented highs.

According to this indicator, the U.S. market is heavily overvalued. The expected return for the future ranges from -0.2% to +0.2%, including dividends. In other words, prices are expected to fall.

On the chart starting before 1980, you can see how exceptional this situation is, and especially how long we’ve been above that green line compared to earlier periods.

That’s why I’m concerned about today’s ETF investors. They expect returns similar to those of the past 10 to 15 years, but this chart clearly shows how exceptional this period has been. Moreover, 74% of those global ETFs are U.S. stocks.

Many investors believe they are investing in a relatively low-risk product because they are “buying the whole market.” But if that entire market is overvalued, I believe the risk of such a product is much higher than the profitable companies in our portfolio, which are currently available for less than their tangible book value.

Another indicator, the Shiller price-to-earnings ratio, is currently at its third-highest level ever.

The reason it hasn't reached the highest level is that today’s very expensive companies are also generating large profits, while a lot of overhyped companies during the dot-com bubble were often loss-making.

Notice the peak in the late 1960s and early 1970s. I’ve written before that I think the current period resembles the Nifty Fifty era more than the dot-com bubble of the late 1990s.

Back then, there was also a group of companies that people thought you could buy no matter the price. Every fund manager jumped on that bandwagon.

The reason was simple: if you didn’t, your fund underperformed, and you risked losing clients who would move their money to a competitor who did hold those stocks. It was purely about keeping your job.

Today, we see a similar story. History doesn’t repeat, but it often rhymes. You can also see what happened to the Shiller PE afterwards, and that drop didn’t come because companies suddenly made a lot more profit.

Now, all wealth managers and large funds are concentrated in the same stocks. This effect is further amplified by passive ETF investors.

But what happens when you keep pushing a ball deeper under the water? At some point, the pressure becomes too great, and it shoots up with tremendous force.

keep repeating it: this is a market with two faces. This is evident from our extensive selection list of buy-worthy stocks. This month, I was once again able to buy a solid, profitable family business at 0.74x its tangible book value.

The contrast is not only visible between large and small companies but also between countries, where the stock market is much cheaper in some than in others.

Using the same calculation as the expected return for the U.S., we see the expected return for:

UK, 8,3%

Australia, 8,2%

Spain, 8,1%

Belgium, 6,7%

In each of these countries, you’ll find both expensive and cheap companies. But these countries provide an interesting starting point for finding undervalued businesses.

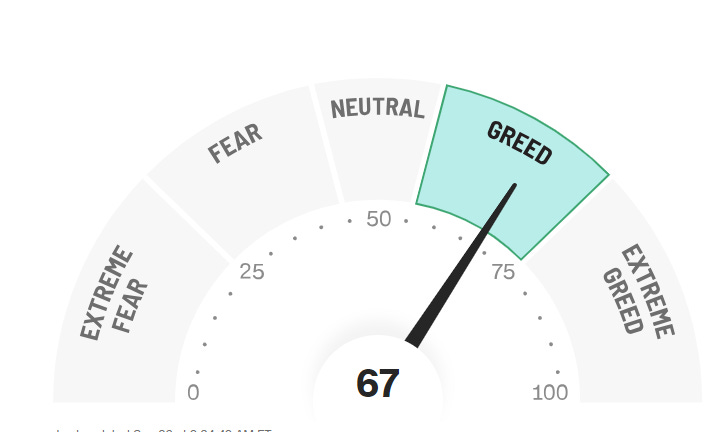

CNN's Fear and Greed indicator is once again showing "Greed," and that's for the entire market, including the cheaper small companies. If they focused solely on the largest companies, which dominate the ETFs, I wouldn’t be surprised if it indicated "Extreme Greed."

A perfect example of the market's schizophrenia is our holding Exor. Last Wednesday, they held their analyst call on the half-year results. Not a single question was asked, and the whole call wrapped up in 20 minutes. There’s simply no interest, despite their stake in Ferrari, which is a market favorite.

Updates this week:

Exor: Ferrari too expensive? The rest too cheap

Hornbach Holding: Stronger than I expected

In Summary: Cloetta, Cake Box, and Stellantis

Transactions Verdubbel Portfolio

Keep reading with a 7-day free trial

Subscribe to Valuing Dutchman to keep reading this post and get 7 days of free access to the full post archives.