Buffett's Farewell

Weekly 19 2025 + Portfolio overview april

This past Saturday felt like a farewell that Buffett allowed us to experience while he’s still alive. I wrote back in February that even his annual letter seemed like a goodbye, and it was, because next year’s letter will be written by Greg Abel.

After last year’s tribute to Charlie Munger, it was once again an emotional moment to say goodbye to Buffett as CEO of Berkshire. He’s held that role for my entire investing career, ever since I started as a complete beginner in 1999. It felt right to say goodbye in person, with a minutes-long standing ovation.

In typical Warren Buffett style, he ended with a quip: the enthusiasm, he said, could be interpreted in two ways.

Let me walk you through a few of the most important messages Buffett shared during the recent meeting, at least, as I experienced them.

Leave Your Emotions at the Door

When Buffett was asked whether the recent market volatility had created opportunities for Berkshire, he gave an answer that explained why I too have been calmly waiting these past weeks instead of rushing to buy.

Buffett said that what happens over the course of 45, or even 100, days means very little. Since he took control of Berkshire, its stock price has dropped by 50% three times, even though there was nothing fundamentally wrong with the company. This current dip? It’s not even close to a major movement.

He referred to the Dow Jones in 1929, which fell from 381 to 42, the equivalent of a drop from 100 to 11. Compared to that, this is nothing. If it bothers you when your stocks drop 15%, then you need a different investment philosophy. Because the world isn’t going to adapt to you, you’ll have to adapt to the world.

In the next twenty years, there will be another extreme event. That’s just how the world works. The world makes big mistakes, and those lead to dramatic surprises, like the financial crisis in 2008. The more sophisticated the systems, the more extreme the consequences.

This is simply part of investing. That’s what makes the stock market a great place for people with the right temperament, and a terrible place for those who panic during drops or get euphoric during highs. You have to leave your emotions at the door if you want to invest.

Balance Sheet First

“Balance sheet first” it’s something I’ve tried to emphasize for years, even if it often goes ignored. Buffett confirmed this during the recent meeting: he looks at eight to ten years of balance sheets before he even checks the income statement.

If a balance sheet isn’t rock solid, then nothing else matters, in his view. And he looks at more than just the numbers, because it’s much harder to hide things on a balance sheet than on an income statement.

For Buffett, having little or no debt is crucial. High levels of debt can create short-term pressure when results temporarily fall short. That can lead to short-term decision-making and limits your ability to seize opportunities when they arise.

He also pays attention to retained earnings. Those profits fund internal growth, and how they evolve tells you a lot about whether capital is being allocated wisely or not.

And of course, there are red flags to watch for, like excessive or overpriced goodwill from acquisitions, or underfunded pension liabilities. As Belgians, we all know the Agfa story.

Naturally, you also need the income statement and cash flow statement for a complete picture. But in the financial world, the focus tends to be on the income statement. By focusing more on the balance sheet, you can really set yourself apart.

Berkshire in Good Hands

After this last meeting, I’m convinced Berkshire is in good hands with Greg Abel. He’s not the charismatic speaker that Buffett or Munger was, but he doesn’t need to be. Think of him more like Tim Cook after Steve Jobs: a capable steward of the company, which continued to perform well under his leadership.

Of course, Berkshire’s sheer size is a disadvantage. But as Buffett said: you only need a few big winners to be a successful investor.

That said, it’s often not clear in advance which ones those winners will be. Even Buffett bought businesses that later disappeared, like Blue Chip Stamps. But it turned out to be a successful investment because the company first generated a lot of cash, which was then used to buy other valuable businesses, even if Blue Chip Stamps itself didn’t stand the test of time.

ValueXBRK

The Berkshire meeting was, of course, memorable. But really, it’s everything around it, the many events and meetings, that make a trip to Omaha truly worthwhile. Even after getting COVID during the trip (either there or en route), I would do it all over again.

For me, ValueXBRK, hosted by Guy Spier (thanks to the team: Chantal, David, Marianne), was a true highlight. One of the speakers was Michael Green. I already wrote about him earlier this year in a weekly update titled “Take the Red Pill.”

It was incredibly inspiring to see him live and even have a brief conversation with him afterward. His views came up again in later discussions. The conclusion remains sobering: the system he describes is a self-reinforcing flywheel, and for now, there’s no alternative. Money keeps flowing into it, which keeps it going and growing.

If that sounds strange, I recommend rereading that earlier piece and watching the accompanying video.

Despite the lack of alternatives, I’m not jumping on the ETF or index investing bandwagon. Buffett said it well: to invest, you have to be able to leave your emotions at the door. For me, that’s only possible when I buy companies that can weather storms, companies I know and understand. Only then can I tolerate volatility.

What might be the major event that triggers the next crash in the coming twenty years, something like the financial crisis or even the Great Depression? It could very well be a collapse of the ETF system.

Until then, I’m not looking for the highest return, but the highest risk-adjusted return. And I’m well aware that one of the biggest risks is myself, my own emotions. That emotional risk is already covered, thanks to our method.

With this approach, we can survive decades of investing. And anyone still standing after decades will naturally be among the best.

This Week

It was a very quiet week in terms of company news, fortunately so, given the events around Berkshire and my illness afterward.

On Tuesday, the lesson in our Introduction to Value Investing series was published: Lesson 12 – Mr. Market.

This coming Tuesday will be busy with various company earnings. Combined with the backlog I’ve built up due to being ill, this means there won’t be a new lesson published next week. The priority remains on our companies.

Doubler Portfolio Overview April 2025

For those not yet familiar with our Doubler Portfolio, read more about it here.

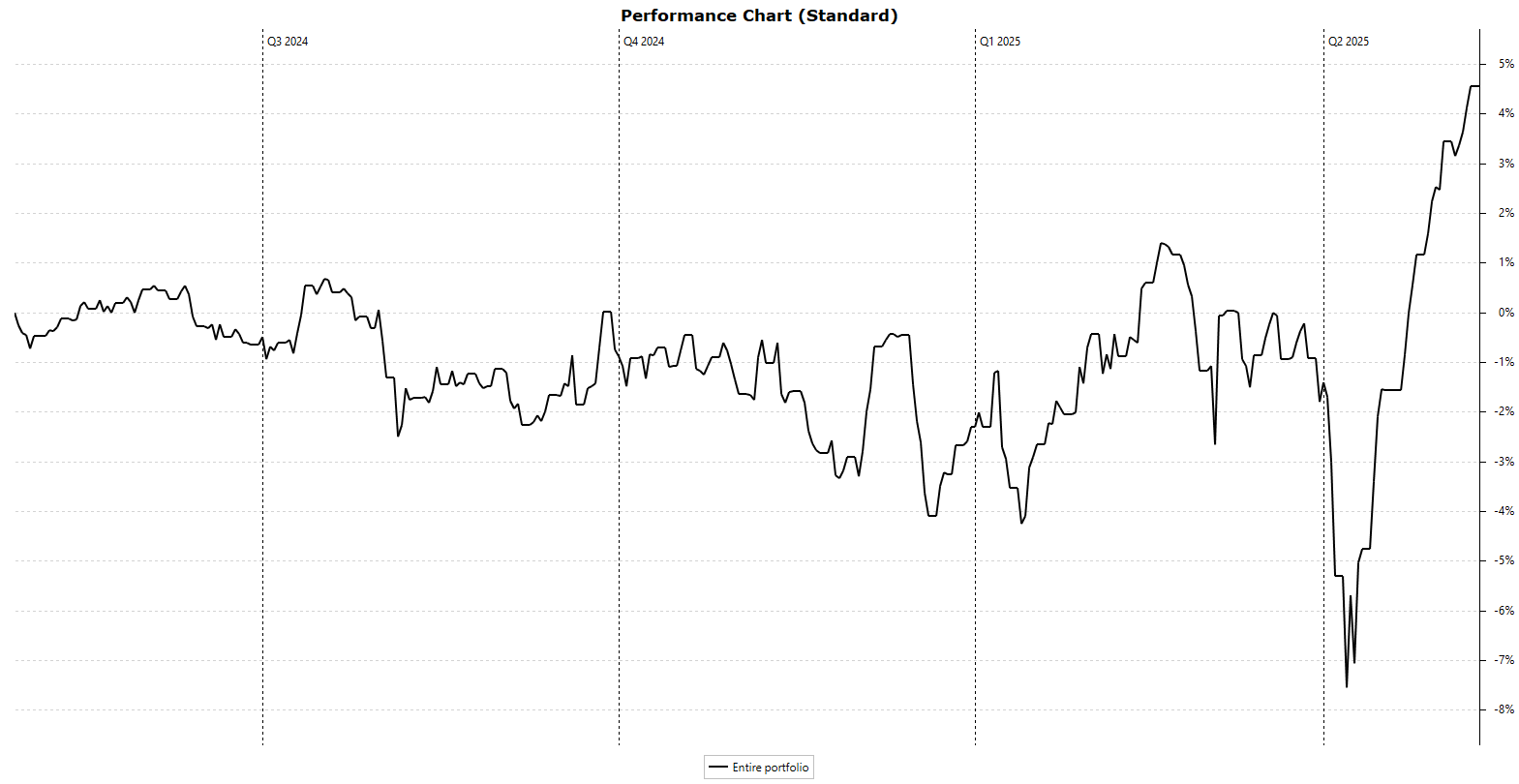

The chart above nicely illustrates how extreme the fluctuations were in April: from +0.93% on April 1 (measured since the start of the year), down to -5%, and finally up to +4.94% by the end of April, and now a bit higher again.

Anyone who went into hibernation in early January and woke up now would think nothing noteworthy had happened during that time.

We should approach this the way Buffett suggests. We don’t need to feel like we missed out on opportunities just because markets dropped 15% in the meantime. Our portfolio fell less, which makes sense given the cash buffer of just under 33% and the fact that our companies don’t have excessive valuations that need correcting. That helps limit the downside.

In short, we’ve got nothing to complain about. It’s exactly twelve months since the Verdubbelportefeuille was launched. With a 2.52% increase through the end of April, it’s not shooting the lights out, but it’s certainly not bad either. Especially when you consider that it’s a portfolio still in the building phase, with a large cash position and deliberately high transaction costs to avoid overtrading.

For comparison: the Euronext 100 rose by 1% in the same period.

These figures also include dividends that you may not have received in your account yet. I count them on the ex-dividend date, even if they haven’t been paid out yet.

April Recap

It continues to surprise me how strong the U.S. markets remain, despite Trump’s tariffs. Since the beginning of January, the S&P 500 is down 3.77%. Of course, I’m pleased that we’re up 7% over the same period. The S&P performed better last year, but since our launch, we’ve managed to narrow that gap to about 4%.

That’s reassuring, especially with 30% still in cash and a portfolio that’s still being built, with deliberately high transaction costs to discourage overtrading.

Let’s once again take a look at the extremes of the past month, the companies that moved more than 10%: