Are you buying shares or companies?

update week 37 2024

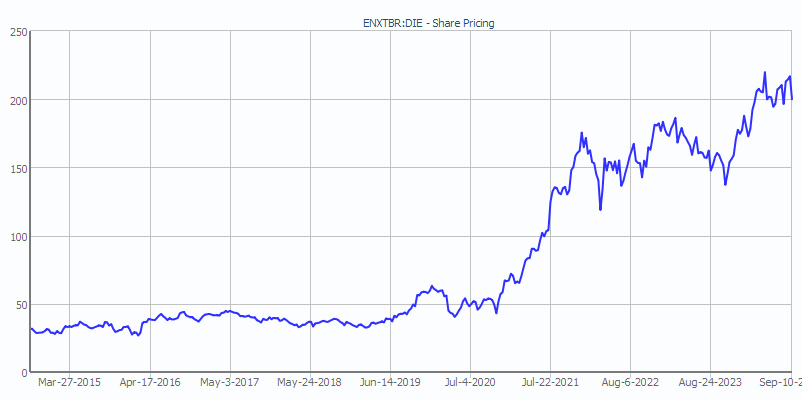

The news that the Belgian holding company D'Ieteren would pay an extraordinary dividend of €74 on a stock price of around €216 was initially met with enthusiasm. That was until people suddenly realised that the €74 would be subject to Belgium’s 30% withholding tax. They force you to take money from one pocket to put it in another. By doing so you effectively pay 10% of your investment in that share directly to the Belgian government.

Personally, I exited D'Ieteren in 2017 when the family made its first inexplicable move.

Why is D'Ieteren doing this? Because the family wants to reorganize; one branch of the family wants to buy out the other. To finance this, they need this money.

To pay this dividend, D'Ieteren itself will take on a significant loan of €1 billion, and its crown jewel, Belron (known for Carglass), will also need to incur an additional €3.8 billion in debt.

In other words, not only does the small investor lose 10% of their capital, but they are also left with a company that is significantly deeper in debt, which limits growth opportunities.

On X (formerly Twitter), I remarked that I don’t always understand investors. Tessenderlo is penalized because Luc Tack is perceived as not being shareholder-friendly, but companies like Euronav and now D'Ieteren, where the majority shareholder literally dips into the minority shareholder's pockets, are not punished. This also raises questions about corporate governance and the role of independent directors, but that is not an exclusively Belgian problem.

I received some comments on this tweet. People argued that Tack does not create shareholder returns. However, the book value of Tessenderlo has grown over the past ten years (under Tack's leadership) by an average of 10.08% per year, while that of D’Ieteren grew by 7.41% per year. That seems like a significant difference in value creation to me.

The growth in profits is harder to compare because, in a holding company like D'Ieteren, it often fluctuates due to a sale or a write-off. At Tessenderlo, cyclicality plays a major role. If I normalize the profits for both companies, I see an average growth of about 11% per year for both.

However, if we look at the stock prices of both companies, we see the following:

The stock price of D'Ieteren rose from €31.7 to €200, even after the decline following the announcement of the special dividend. This equates to a return of 531%.

However, the stock price of Tessenderlo only increased from €21.95 to €24.4, resulting in a return of just 11% over ten years.

Then it became clear what was meant by shareholder returns: capital gains. However, that is not the value creation or type of return I am looking for as a shareholder (distributed profits + value growth).

This also touches on the core of how one views the stock market: do you buy shares as products to trade, or do you buy shares as proof of ownership in underlying companies?

That Tessenderlo performed better fundamentally is evident from the growth in its book value. Another explanation for the difference in stock price growth could be that D'Ieteren was undervalued at the time, and Tessenderlo was overpriced.

There’s something to that because D'Ieteren was trading at a price-to-earnings ratio of 15.4 and a price-to-book ratio of 1.01 back then. That’s not expensive at all, but not a bargain either.

Tessenderlo, on the other hand, was trading at 17 times earnings and 2.39 times book value. That was certainly not cheap, but in 2014 there was euphoria over the fact that Tack had taken the company off the hands of the French government to get it back on track.

What do we see today? D'Ieteren is trading at 28.1 times earnings and 2.87 times book value. In other words, investors are now willing to pay significantly more for D'Ieteren. For Tessenderlo, investors today are only willing to pay 0.78 times book value and around 7 to 8 times normalized earnings, which is considerably less than ten years ago.

Both companies have grown, but for one company, investors today are willing to pay 184% more for the underlying book value, while for the other company, they are willing to pay 67% less. Or, calculated based on normalized earnings: investors are willing to pay 82% more for one company and 53% less for the other.

In other words, the stock price increase at D'Ieteren was largely due to other investors’ willingness to pay more. Of the 531% stock price increase at D'Ieteren, about 200 percentage points can be attributed to the company's growth; the remaining 331 percentage points are due to a shift in sentiment.

In contrast, negative sentiment is heavily weighing on Tessenderlo’s stock price. As we previously established, Tessenderlo grew faster than D'Ieteren.

Attributing Tessenderlo’s weak stock performance to the so-called "shareholder-unfriendly" majority shareholder seems too simplistic. Compared to D'Ieteren, Tack is a gift because by buying back shares at around €24 each, he enriches all shareholders, not the Belgian government.

D'Ieteren could have also chosen to buy the shares of the family member through share buybacks (under certain conditions), but then the remaining family shareholder would control only 46.18% of D'Ieteren, instead of 50.1%. That immediately explains why the small investor bears the cost.

Back to what’s important for us: we’ve received new figures from several of our companies, including another holding.

Updates this week: